With the longer term impact of COVID-19 as yet one of the unknowns, there has been recent news regarding disclosure requirements for SMSF trustees who have not yet completed their 2019 financial year accounts.

We’ve seen some recommendations related to the need to disclose the pandemic as a significant event in the “Events subsequent to Balance Date”.

Accountants should be having a discussion with the trustees for SMSF who have not yet completed their 2019 financial year accounts, and at the same time it might also be necessary to consider the disclosure of COVID-19 additionally in the 2020 financial year.

There is value in communicating with SMSF Trustees for whom you have already completed the 2019 return, and let them know even though the return is completed and lodged, had it not been lodged there should have been consideration of a disclosure of COVID-19 in the 2019, and it might also be necessary to consider the disclosure of COVID-19 additionally in the 2020 financial year.

With respect to SMSF audits, there is the expectation that the SMSF auditors will be including additional clauses in the 2019 SMSF audits they have yet to start, and the additional clause should draw the attention to the potential impact of COVID-19.

There are lots of issues to consider for Australian accountants who have clients with Self Managed superfunds.

If you’re a little overwhelmed with the SMSF administration or audit for your clients, then please reach out to Odyssey. We annually complete some 7,500 SMSF financial year accounts for Australian accounting firms as well as 5,000 SMSF audits for our SMSF auditor clients.

The 7 top challenges in auditing SMSF’s over the next decade

The 7 top challenges in auditing SMSF’s over the next decade

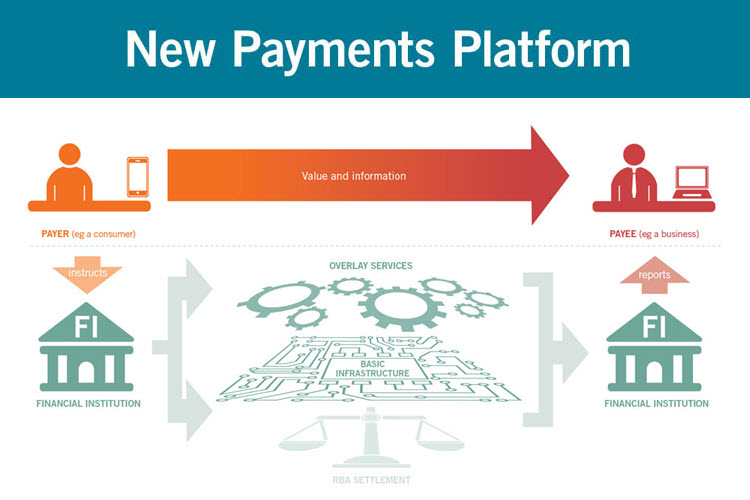

NPP Disruption in real time payments coming this year…

NPP Disruption in real time payments coming this year…

Simple Australian “I” returns disappear from Australian Accountants’ Compliance work

Simple Australian “I” returns disappear from Australian Accountants’ Compliance work

Finding work life balance for Australian accounting firm owners

Finding work life balance for Australian accounting firm owners

What Australian accounting directors fear most about Outsourcing…

What Australian accounting directors fear most about Outsourcing…

2019 – It’s a New Year!

2019 – It’s a New Year!